What Most People Get Wrong About Annuities

June is Annuity Awareness Month, so let’s close it with a truth:

What you heard may not be the whole story.

Annuities have a reputation.

Some of it is fair.

Some of it is old.

Some of it came from a bad product, a bad fit, or a bad explanation.

But one story should not make the whole decision for you.

Annuities are not all built the same way.

Some are used for income.

Some are used for protection.

Some are used for growth with limits.

Some are not a fit at all.

That is why the conversation needs more clarity before it gets a quick yes or no.

This week, we are busting a few myths so you can understand the difference between what people repeat and what may actually apply to your retirement plan.

👇🏾Let's hop in.

The Wealth Minute

Myth: Once Your Money Goes Into an Annuity, You Can Never Touch It Again

This is one of the biggest fears people have about annuities.

They hear “annuity” and think:

“My money is locked away forever.”

That is not the full story.

Annuities are contracts.

And contracts have rules.

There may be a surrender charge period.

There may be limits on how much you can withdraw each year without a penalty.

There may be reasons moving the money too soon does not make sense.

But that is different from saying you can never touch your money again.

The better questions are:

💫What kind of annuity is it?

💫How long is the contract?

💫What access does it allow?

💫What happens if I need income or a withdrawal?

So the myth is not true.

Putting money into an annuity does not automatically mean you can never touch it again.

The real issue is access.

How much?

How soon?

At what cost?

That is what you want explained before you decide.

💬 Mindset Shift: Before you reject the annuity, understand the access.

🕊️ Faith Note: Proverbs 4:7 reminds us that wisdom begins with understanding. Before you reject something or accept it, make sure you understand what you are agreeing to.

Bottom Line: Your money is not automatically locked away forever. First, learn how access works.

Wealth Moves

Write down the sentence you keep repeating about annuities.

Then ask:

“Do I know this, or did I hear this?”

That is it.

Before you accept or reject the conversation, separate fact from rumor.

The Freedom Path

Do Not Put Short-Term Money in a Long-Term Job

Here is where people get into trouble.

They put money in the wrong place and then blame the tool.

Money you may need soon should not be treated like long-term money.

That is true with annuities.

But it is also true with retirement accounts, CDs, real estate, life insurance, and even business money.

The problem is not always the product.

Sometimes the problem is that the money was given the wrong job.

Do you need:

💰Quick access.

💰Income generated later.

💰Protection.

💰Growth.

💰Debt elimination.

But do not ask the same dollar to be fully liquid, fully protected, fully growing, and fully available at the same time.

That is where confusion starts.

Before you choose the tool, name the job.

💬 Mindset Shift: The wrong tool can make a good strategy feel like a mistake.

🕊️ Faith Note: Proverbs 24:3 says a house is built by wisdom. The same is true for money. Order matters.

Bottom Line: Access problems often start when short-term money is put into a long-term job.

Wealth Moves

Do a 90-day access check.

Ask yourself:

“If I needed money in the next 90 days, where would I get it?”

Write down your first three sources.

Then mark each one:

Easy access Possible, but costly Not meant for short-term use

That will show you something quickly.

If your emergency plan depends on money that is hard to access, expensive to touch, or meant for retirement income, that money may be carrying the wrong job.

Access needs to be planned before pressure shows up.

Coffee Chat Question

If we were to meet for coffee, what would you want to know?

Feel free to email me questions that will anonymously be added to this section during each edition.

“Lisa, what problem does an annuity actually solve?”

That is a great question.

An annuity is not your emergency fund.

It is not your checking account.

And it is not where every retirement dollar belongs.

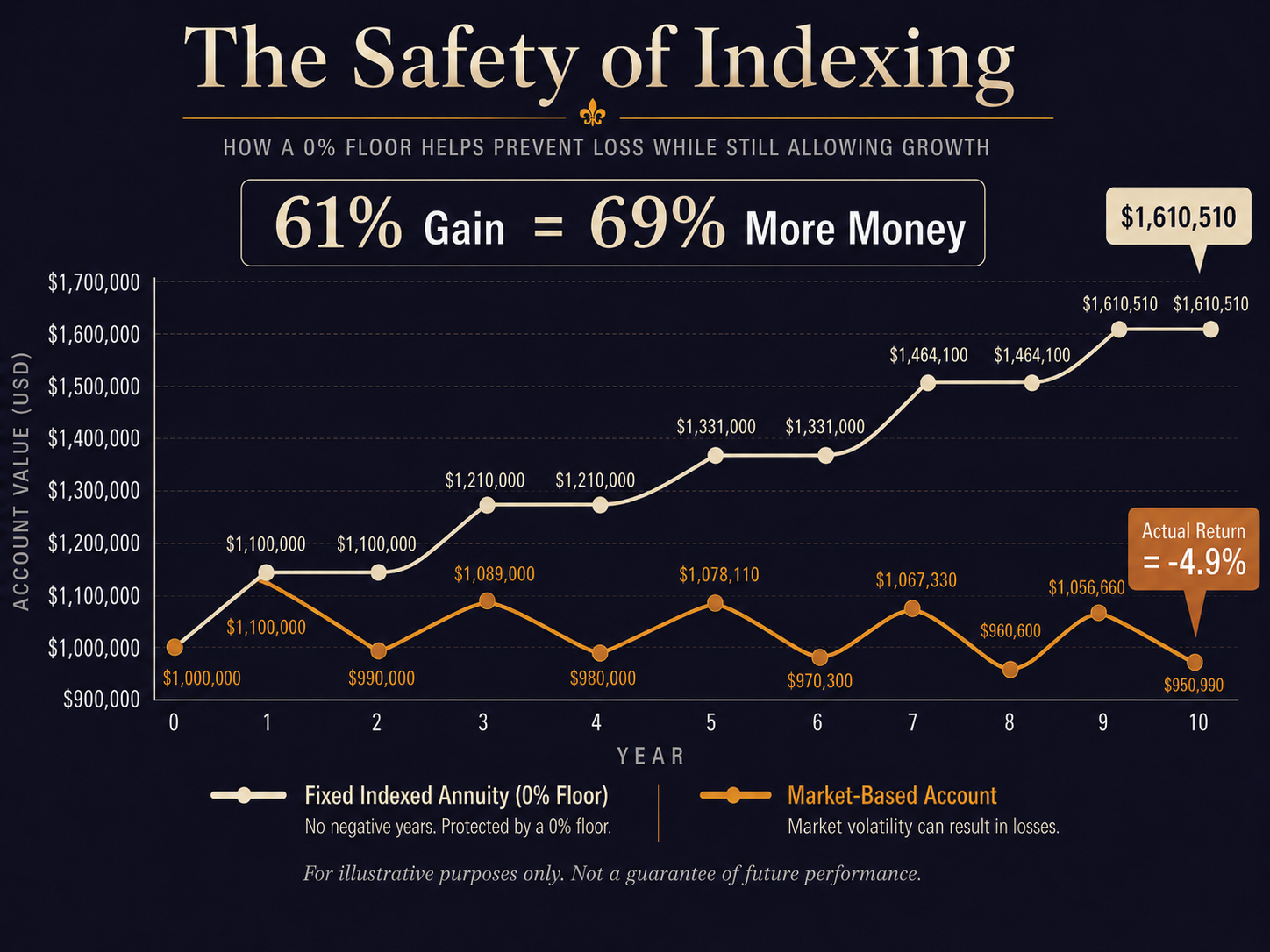

The Safety of Indexing

This illustration shows how a fixed indexed annuity with a 0% floor may help protect retirement money from market loss while still allowing room for growth. The market-based account moves up and down with volatility, including loss years. The fixed indexed annuity line shows no negative years because the floor helps protect against market downturns.

This is not about saying one tool solves every problem. It is about showing one problem a fixed indexed annuity may help solve: protecting part of your retirement money from losses that happen too close to when you need income.

For illustrative purposes only. Not a guarantee of future performance. Product features, caps, participation rates, fees, surrender charges, and crediting methods vary by annuity contract.

But the visual above shows one problem a fixed indexed annuity can help solve:

market loss near retirement.

The market-based account goes up and down.

The fixed indexed annuity has a 0% floor, so it does not take the same loss in down years.

That matters when the money is close to needing a paycheck job.

So do not start with:

“Do I need an annuity?”

Start with:

“What problem am I trying to solve?”

If the problem is short-term access, an annuity may not be the tool.

If the problem is lifetime income, protection, or reducing market timing risk, then it may belong in the conversation.

That is the difference.

A tool only makes sense when it matches the job.

💬 Mindset Shift: Do not start with the product. Start with the problem.

🕊️ Faith Note:Proverbs 20:18 reminds us that plans are established by counsel. Wise planning names the issue before choosing the tool.

Bottom Line: An annuity does not need to solve everything. It needs to solve the right thing.

⚡ Your Next Right Move

As Annuity Awareness Month closes, do not let an old opinion make a current decision.

If you have money sitting in an old 401(k), TSP, 403(b), or IRA, ask:

“Is this money protected from the kind of loss I cannot afford to take?”

Because a loss is not just a loss when retirement is close.

It can change the paycheck.

It can change the date.

It can change the confidence.

Start the Safe Retirement Blueprint

🕊️ Faith Note: James 1:5 reminds us that if we lack wisdom, we can ask for it. Money decisions do not require panic. They require wisdom, clarity, and the willingness to ask better questions.

Because what you heard may not be the whole story.

And the right question can change the whole conversation.

Stay Awake Out There,